2026-03-11 Afternoon Stock Report

Market Overview

- Regime: Volatile / Geopolitical Pressure

- Key drivers: Escalating US-Iran conflict, skyrocketing crude oil prices (Brent near $90), and a surge in the 10-year Treasury yield to 4.23% (highest in nearly a year).

- Risk flags: Stagflation concerns as energy prices spike while CPI remains above target (2.4%). Tech and growth sectors are sensitive to the rising cost of capital.

High-Priority Setups

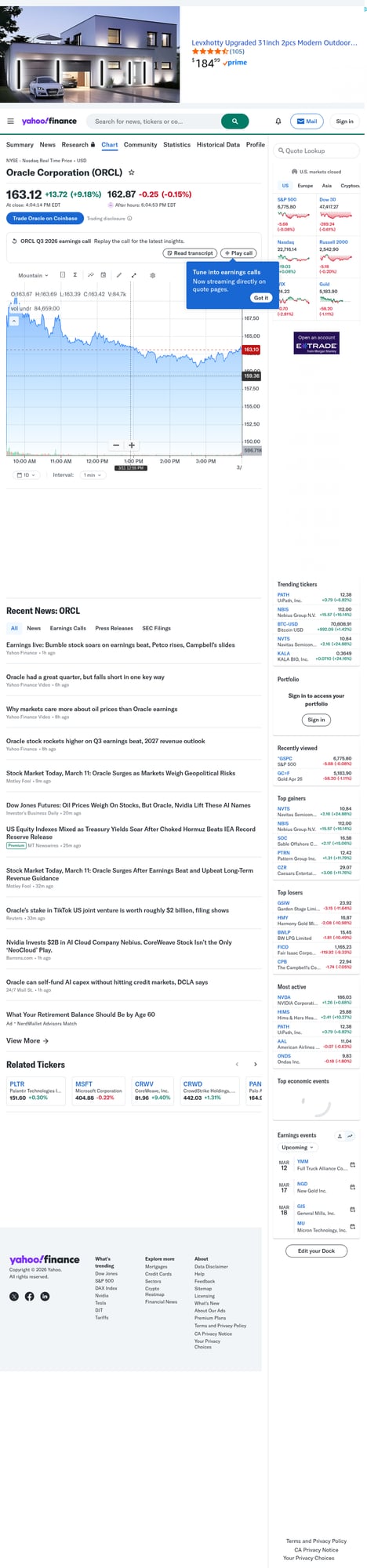

- ORCL (Oracle Corporation)

- Thesis: Strong AI and Cloud demand decoupling from macro headwinds.

- Catalyst: Q3 earnings beat + 20% revenue growth + upbeat 2027 guidance.

- Risk: Aggressive AI capex spending and broader tech sell-off.

- Bias: Bullish (momentum leader).

- Invalidation: Close below $155.

- Chart:

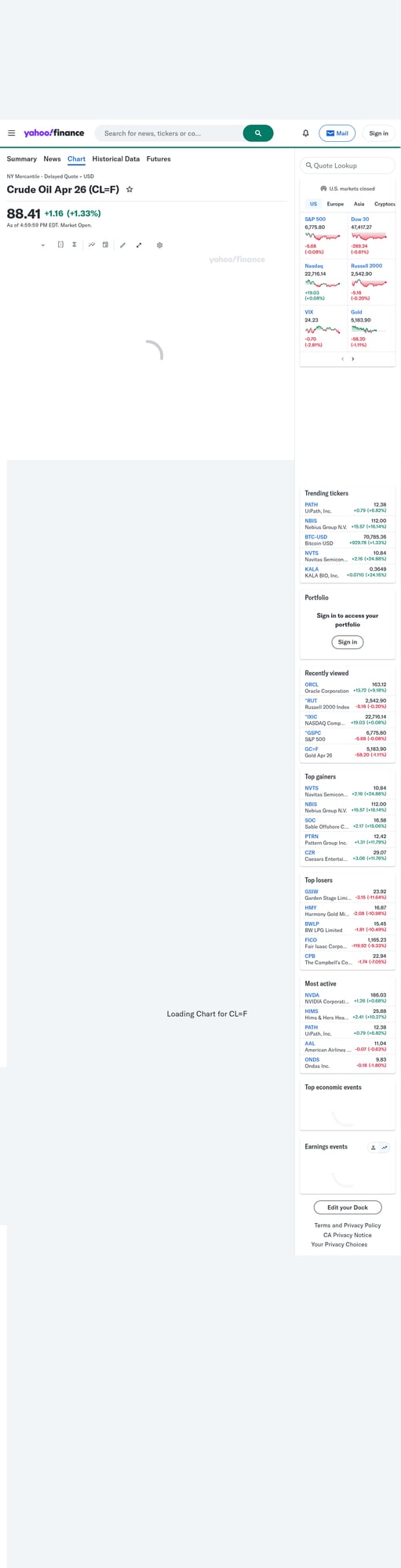

- OIL (Crude Oil Futures)

- Thesis: Supply shock due to the closure of the Strait of Hormuz.

- Catalyst: US strikes on Iranian infrastructure + geopolitical risk premium.

- Risk: Global release of emergency reserves.

- Bias: Bullish (parabolic).

- Invalidation: De-escalation headlines or Brent below $82.

- Chart:

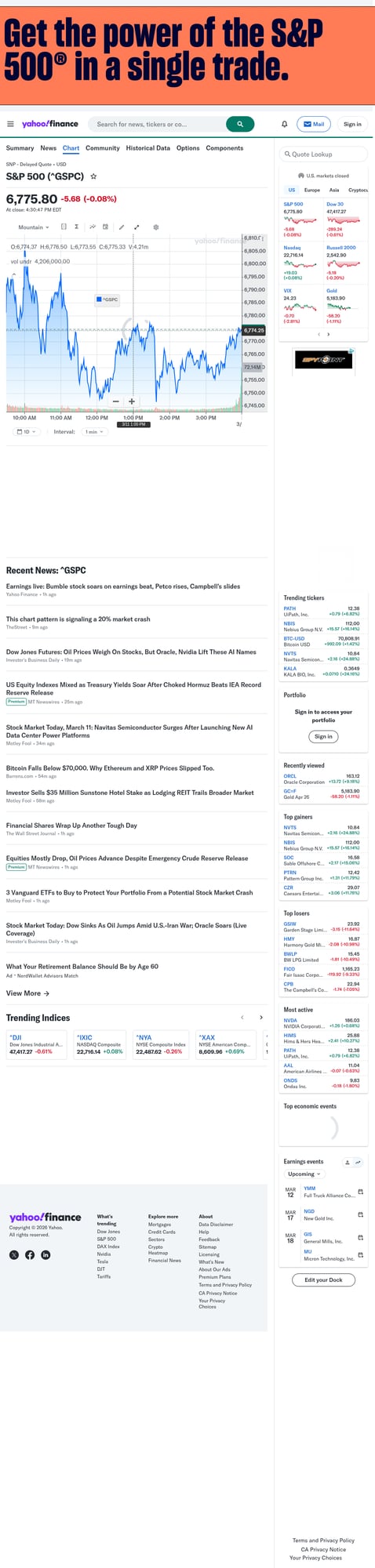

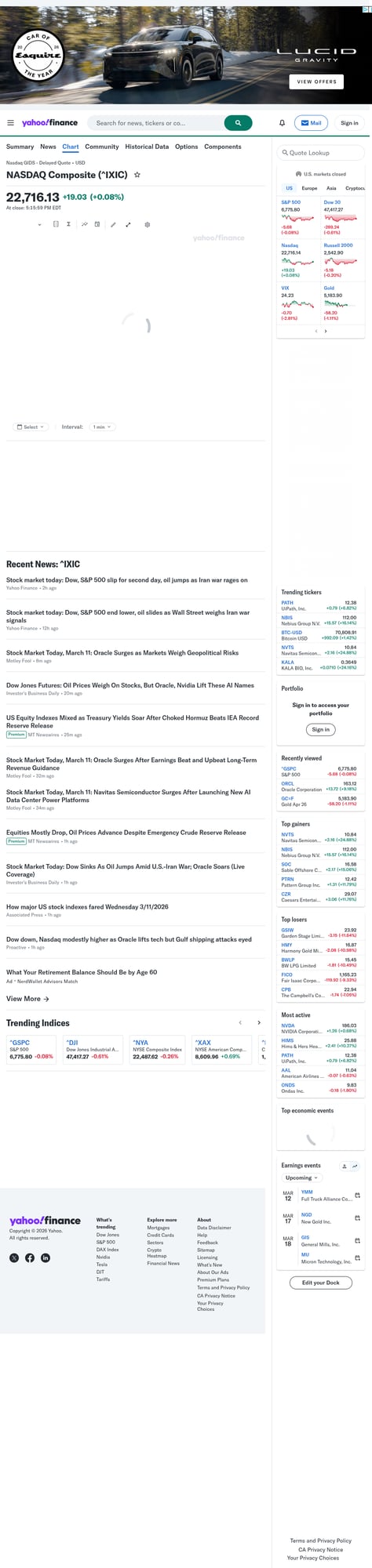

Market Context (Indices)

- SPY (S&P 500): Slipped 0.10% as oil gains were offset by yield pressure.

- QQQ (Nasdaq): Edged up 0.08% thanks to Oracle and Nvidia support.

- IWM (Small Caps): Flat at -0.02%, struggling with higher-for-longer yield narratives.

Watchlist / What Changed Today

- NVDA: Held firm despite macro weakness, buoyed by the “Oracle effect” on AI cloud demand.

- PATH: Surged 6.8% on high relative volume; seeing strong momentum in AI-adjacent software.

- Yields: 10-year Treasury hitting 4.23% is the primary headwind for equities.

Bottom Line

The market is currently a “tale of two tapes”: Oil and Geopolitical hedges are surging, while AI leaders like Oracle provide a floor for tech. Broad indices remain vulnerable to further yield spikes. Focus on relative strength leaders (ORCL, NVDA) or direct energy plays.